About this Hardcover

- ISBN-13

- 9781119903802

- Author

- Cyril Shmatov,Cino Robin Castelli

- Publisher

- John Wiley & Sons

- Edition

- 1

- Published

- 2022-12-01

- Pages

- 240

- Binding

- Hardcover

Verified US edition — ISBN 9781119903802

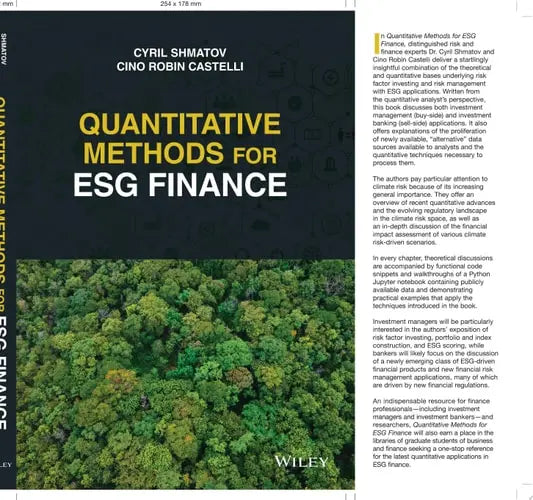

ISBN 9781119903802 identifies the 1 of Quantitative Methods for ESG Finance by Cyril Shmatov by Cyril Shmatov,Cino Robin Castelli, published by John Wiley & Sons (2022-12-01). Every copy Book Shop Now ships against this ISBN is the genuine US-edition print run from the original publisher's authorized US distribution — no overseas reprints, no scanned facsimiles, no "international edition" rebranding. Verify this ISBN against your professor's syllabus before checkout.

About John Wiley & Sons

John Wiley & Sons publishes academic and professional reference books across business, sciences, engineering, and education. Wiley's medical journal back-titles, biostatistics references, and professional design textbooks (Piotrowski's Professional Practice for Interior Designers, Wiley Finance series) are widely course-assigned. Book Shop Now sources Wiley US editions directly to maintain ISBN verifiability.

How students use this book

NCE, CPCE, and state counseling licensure exams test across nine content areas — human growth, social/cultural, helping relationships, group work, career, assessment, research, and professional orientation. This title works best inside a multi-resource prep plan: a content review like Rosenthal's, a Q-bank, and audio review for commute time. Most successful candidates dedicate 8-12 weeks of focused review across all nine domains.

How Book Shop Now sources this title

Every book Book Shop Now ships is sourced directly from US publishers or their authorized US distributors — never from overseas grey-market resellers, marketplace commingled inventory, or scanned facsimile reprints. We do not sell "international edition" copies relabeled as US editions, and we do not accept loose-leaf substitutions for hardcover orders. Each shipment is inspected against the listed ISBN before dispatch, ships from US warehouses with 1-3 business day handling, and is covered by a 14-day return policy on books that arrive damaged or mismatched. Read our guide to spotting counterfeit textbooks →